How Much Will My Taxes Increase if the Cape Elizabeth School Bond is Approved?

Updated April 9, 2025

If the school bond is approved on the June ballot, when do we start paying for it?

You may be wondering so that you can plan ahead for any changes to your property tax bill. Therefore, it’s important to know that the school bond would not impact taxes until FY2027, or your October 2026 tax bill, giving you time to anticipate the increase. The increase is also spread out over 6 years and will not hit your tax bill all at once.

Per the town manager, the schedule will be:

Source: Town Council Special Meeting, April 7, 2025

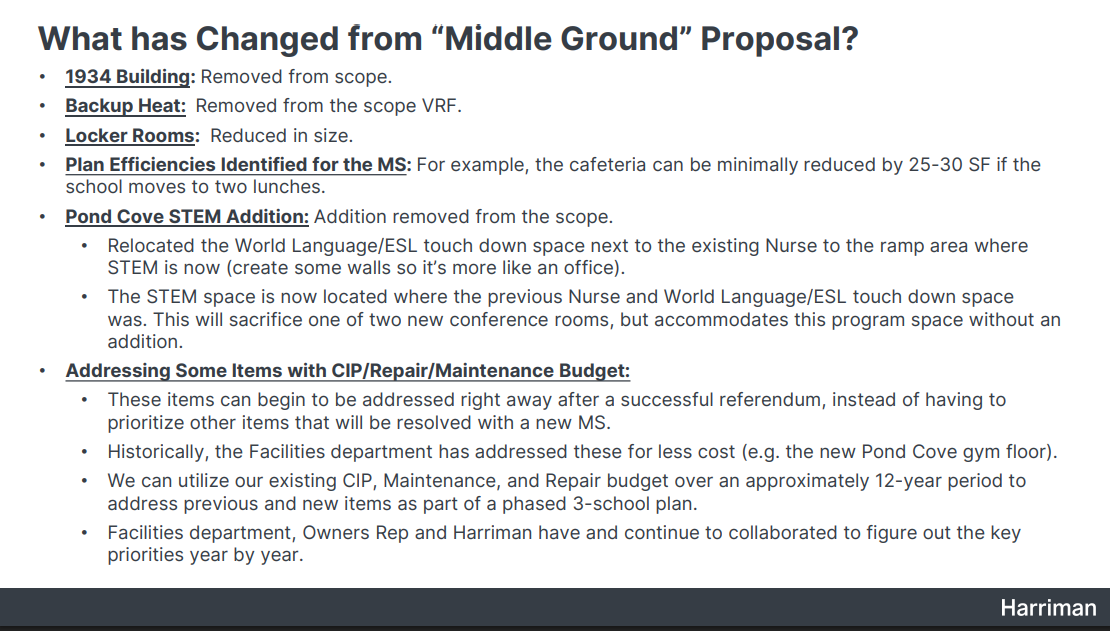

How does this $86.5 million project differ from the $94.7 million project from November 2024?

After the Middle Ground proposal failed in November 2024 by a vote of 48.8% to 51.2%, the School Board revisited the proposal with Harriman architects to find areas to reduce the scope of the construction, shave some square footage from different areas of the building, and spread out projects over the next decade through the district’s Capital Improvement Plan.

A Capital Improvement Plan (CIP) is also referred to as a maintenance/repairs budget. This is a line item already included in the annual school budget, and is entirely locally controlled and does not fluctuate with state or federal funding. A CIP account can be thought of as a savings account built over time, so you can pay for repairs out of your operating budget. It is NOT a separate bond or additional tax increase.

Here is a sample of some (but not all) of the projects that would be completed under this budget over the next 8-12 years:

It’s important to note that most of the projects on this list, like replacing flooring, are actually cheaper to do with your regular maintenance budget because you can hire a local, specialized contractor or handle it in-house. If you try to complete the same project with a full construction firm, the cost is generally much higher because of all of the additional overhead.

How does a municipal bond work?

A bond is essentially a way for a town to borrow money to fund large projects, like building schools or upgrading infrastructure, in a structured and manageable way.

When voters approve a bond, they authorize the town to spend up to a certain amount—in this case, $86.5 million. However, the town doesn’t get all that money immediately, nor can it spend beyond that limit without returning to voters for permission. Instead, the town works with bond agents to issue bonds in smaller amounts as needed, typically spread out over time. For example, the town might issue two or three separate bonds, matching the timing of when the money is actually required for the project, just like paying in installments for a contractor for your house—half at the start of a project and the remainder at the end.

This staggered borrowing approach is why the property tax increase is spread out over several years as shown in the above table. Since the town doesn’t take on the full $86.5 million in one go, the tax impact is also gradual. Additionally, if the project comes in under budget, large donations are received, or interest rates fall, the full increase estimated above may be higher than the actual amounts.

How does this bond impact the bigger picture of the town’s financial position?

Overall, Cape Elizabeth is in a strong financial position for infrastructure improvements. The town currently has S&P’s highest and best bond rating at AAA and Moody’s second best at Aa1, which is the highest given to a town of our size. This means we can borrow at the most favorable interest rates.

Joe Cuetara of Moors & Cabot Investments, the town’s bond council, presented to the Town Council in 2022 and shared that the town is in a strong financial position, but at risk of slipping in the eyes of bond investors due to deferred maintenance and aging infrastructure.

“Cape Elizabeth’s debt service as a percentage of expenditures at 3.64%, is considered very low. Moderate, according to the S&P is between 8%-15%. Having less than this range suggests that, ‘You are letting your infrastructure deteriorate, letting your assets fallow and creating greater problems and expenses in the future,’ Cuetara said.

Fund balances higher than 12% suggest over-leveraging. Cape Elizabeth’s overall net debt per capita at $978, “Is incredibly low in terms of your ability to borrow if you want to,” he added. The median in Maine is approximately $3000.

Borrowing, Cuetara explained, allows you to “borrow an asset for 20 years” and is “less of an evil in terms of spreading the useful life of the asset and benefits are received by the users of the asset.

Overall net debt as a percentage of market value is considered moderate when it is between 3%-6%. Cuetara said, “Above 3% is a warning; below 3% makes you wonder if you are maintaining infrastructure?” Cape Elizabeth’s overall net debt as a percentage of market value is 0.35%.”

Municipal debt, like a bond, is not inherently bad—in fact, it can be a smart way for towns to invest in long-term infrastructure while keeping property taxes steady. Think of it as being similar to a homeowner using a home equity loan to remodel their kitchen. Once the kitchen is paid off, the homeowner might use the same monthly payment structure to fund a bathroom remodel. This approach allows for continuous improvement without major disruptions to the household budget.

Towns operate similarly but on a much larger scale. For example, when a bond for a new library is paid off, the town can maintain property taxes at the same level and use the freed-up funds to finance a new project, like an addition to the fire station. This strategy ensures that the town is consistently investing in infrastructure without sudden spikes in taxes.

Unfortunately, our town hasn’t been following this approach. When the library principal was paid down, the funds were used to reduce taxes rather than reinvest in new projects. While this may sound good in the short term, over decades it has contributed to underinvestment in critical repairs and improvements. The town now faces a situation where one project can lead to a sharp increase in property taxes instead of a smoother, gradual increase.

Our new Town Manager is working to implement a better approach to long-term planning, but it will take time to course correct.

How does the town revaluation impact my taxes?

The town-wide revaluation reassesses property values to reflect current market conditions, ensuring a fair distribution of the tax burden based on up-to-date property values. Revaluations are “tax neutral”, because the town’s budget does not change. What changes is the allocation of payment among households. For more in-depth information on how revaluation works, visit our comprehensive blog post.

To see your property value and tax amount before the town-wide revaluation:

Go to the Tax Assessor’s Database

Type in your last name and hit ‘search’. If no results are found, try searching for your street number and name without your last name.

Scroll down to “Tax Bills” and download the 2023-2024 bill.

Your pre-revaluation property value is listed on the top right, next to “Total Value”.

Your pre-revaluation property tax amount is listed next to “Total Tax” in the same box.

To see your property value after the town-wide revaluation:

Go to the Tax Assessor’s Database

Type in your last name and hit ‘search’. If no results are found, try searching for your street number and name without your last name.

Scroll down to “Tax Bills” and download the 2024-2025 bill.

Your post-revaluation property value is listed on the top right, next to “Total Value”.

Your post-revaluation property tax amount is listed next to “Total Tax” in the same box.

Alternative way to see the difference between your taxes before and after the revaluation:

The Tax Assessor has also provided this report to view your taxes before and after. It’s important to remember that as part of this process, the previous mill rate of $22.34 has decreased to $11.00.

Tax relief options are available to you.

Below, you’ll find a list of common tax relief options that you may qualify for, but there is still more the Town Council can do to support our most vulnerable neighbors.

Homestead Exemption

The homestead exemption provides a reduction of up to $25,000 in the value of your home for property tax purposes, meaning you can save ~$275 on your next tax bill. To qualify, you must be a permanent resident of Maine, the home must be your permanent residence, you must have owned a home in Maine for the twelve months prior to applying. Learn more and apply here.

Cape Elizabeth’s Senior Tax Relief Program

Eligible applicants can save up to $1,500/year. Must be 65 years or older; Be a property owner within Cape Elizabeth for ten years or greater; Have a homestead exemption; Have a federal AGI of less than $70,000; and Have taxes greater than five percent of their gross adjusted taxable income. Learn more and apply here.

Veteran’s Exemptions

A veteran who served during a recognized war period and is 62 years or older; or, is receiving 100% disability as a Veteran; or, became 100% disabled while serving, is eligible for $6,000. Apply here.

Property Tax Fairness Credit

Eligible Maine taxpayers may receive a portion of the property tax or rent paid during the tax year on the Maine individual income tax return whether they owe Maine income tax or not. Learn more here.

State Property Tax Deferral Program

A lifeline loan program that can cover the annual property tax bills of Maine people who are ages 65 and older or are permanently disabled and who cannot afford to pay them on their own. It allows for repayment of the loan once the property is sold or becomes part of an estate. Learn more here.

Thomas Jordan Trust

The Thomas Jordan Trust is a local resource administered by the Town of Cape Elizabeth to help citizens. To apply, use the online PDF application or call 207-799-7665 during normal business hours. Learn more here.

What neighbors are saying…